Information presented on this web page is intended for informational and educational purposes only and is not meant to be taken as legal, financial, investment or tax advice. We do not accept any responsibility for any trading or investment related losses. Please review our disclaimer on before taking action based upon anything you read or see.

When preparing your finances, especially for retirement, the Present Value of Annuity Calculator may be helpful. Your savings and Social Security benefits will be your main sources of income after you’ve stopped working, allowing you to enjoy your later years. An extra income stream is produced by buying an annuity, which may simplify things. Many individuals consult with a financial adviser to tailor a plan to their retirement objectives. However, the Present value of the annuity calculator would be of great use to you if you need more flexibility.

You can also determine the current value of a series of future cash flows with the aid of the present value of the annuity calculator. These cash flows are produced by a financial product called an annuity.

The user-selected discount rate, such as a planned return on investment or the current market interest rate, determines the current value of the cash flows. You may acquire financing on the open market at this rate of interest. The risk-free return on investment would be the lowest discount rate used.

Read More: How to Live off Investment Interest

Additionally, the user may choose a price for the annuity based on the calculated present value. Come along as we highlight more on the Present Value of the Annuity Calculator.

What is a Present Value of an Annuity?

The amount of money required today to cover a series of prospective annuity payments is the annuity’s current value.

An amount of money received now is worth more than a similar quantity later due to the time value of money. Using a present value calculator, estimate if you’ll get more money by accepting a lump amount now or an annuity stretched out over some years.

Additionally, an annuity is a deal you sign with a financial institution in return for payments in the future.

The monetary worth of your future installments is the present value of an annuity. The calculation includes the rate of return or discount rate. Future payments on an annuity are decreased depending on the discount rate. Therefore, the present value of the annuity decreases as the discount rate rises.

How to Calculate the Present Value of an Annuity?

Using the P.V. of an annuity due, the following methods may be used to determine the present value of an annuity reimbursement:

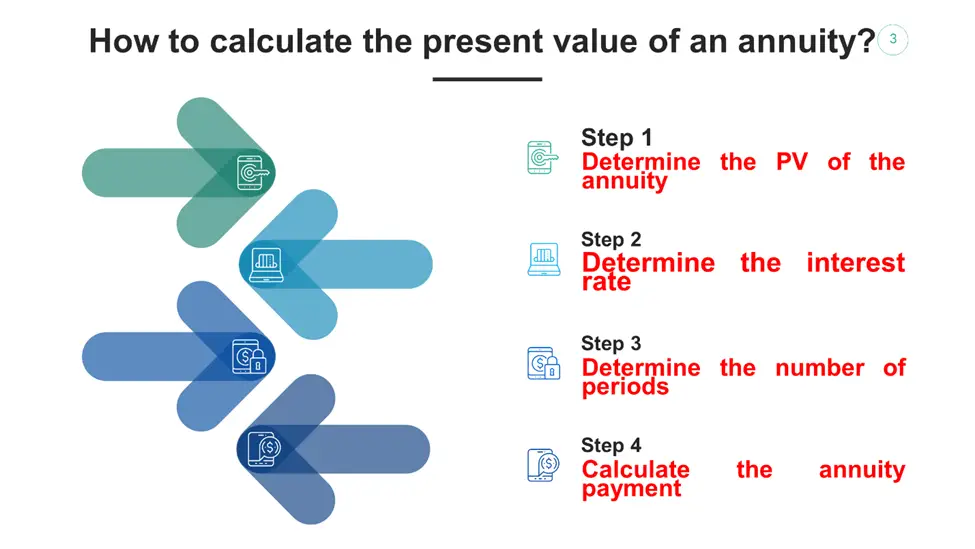

Step 1: Determine the P.V. of the annuity

First, figure out the annuity’s P.V. and make sure the payment will be paid at the start of each month. PVA Due serves as a marker.

Step 2: Determine the interest rate

The interest rate should then be calculated using the current market yield. The annualized interest rate is then divided by the periodic payments each year to get the effective interest rate. And r indicates it.

More Resource: Loan Interest Calculator

R is equal to the annualized interest rate divided by the number of monthly payments.

Step 3: Determine the number of periods

Next, multiply the number of regular payments by the number of years to get the number of periods. And n indicates it.

N = Years x Number of Regular Repayments in a Year

Step 4: Calculate the annuity payment

The last step is to compute the annuity payment based on the P.V. of the annuity due using the steps above: P.V. of the annuity due (step 1), effective rate of interest (step 2), and various durations (step 3).

In summary, the following equation determines the present value of a regular annuity:

Regular cash payments x ([1-(1+Interest rate)] (Payments made) / (Interest rate)

Present Value of Annuity Calculator

Examples of P.V. of Annuity Calculation

Some Examples of P.V. of annuity calculation include:

Example 1:

Let’s use David as an example. David won a $10,000,000,000 jackpot. He chose the payout option of an annual annuity payment for the subsequent 20 years. Calculate David’s annuity payout if the market’s constant interest rate is 5%.

The information needed to calculate annuity payments is provided below.

$10,000,000,000 PVA Ordinary Moreover, the annuity will be paid out the year.

As a result, the following may be used to calculate annuity payments using the formula:

Annuity: [1 – (1 + 5%)-20] / 5% * $10,000,000

Annuity is equal to $802,425.87 $802,426.

As a result, David will make annuity payments totaling $802,426 for the next 20 years.

Example 2:

Mr. Johnson, a 65-year-old retired veteran of the military, has been making monthly contributions to his retirement account for the last 30 years. And he can finally begin taking money out now.

In exchange for signing the contract, the retirement firm will provide him a one-time payout of $500,000 or $30,000 on January 1st for the next 25 years. To choose the best course of action, he needs to know what the $30,000 in annual payments would be worth today.

According to the present value calculation above, the annuity payments are worth around $400,000 today. Assuming a 6 percent average interest rate, this is true. Therefore, Mr. Johnson would be better off investing the lump sum money himself now.

Why is the P.V. of Annuity important?

The ability for investors to compare assets across time makes present value crucial. P.V. may assist investors in evaluating the potential financial gains from present assets or liabilities.

The present value of an annuity may be calculated by investors based on its expected future returns, and it is also used in financial forecasting, capital budgeting, and bond trading.

For instance, when comparing two different investment kinds, an investor might determine which one delivers the highest returns by comparing their current prices.

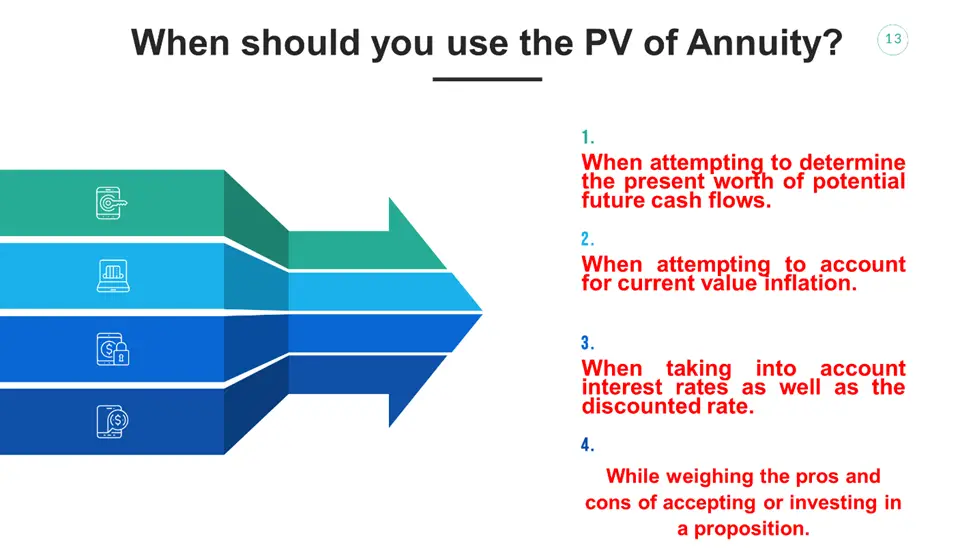

When should you use the P.V. of Annuity?

You can use the P.V. of Annuity in the following scenarios:

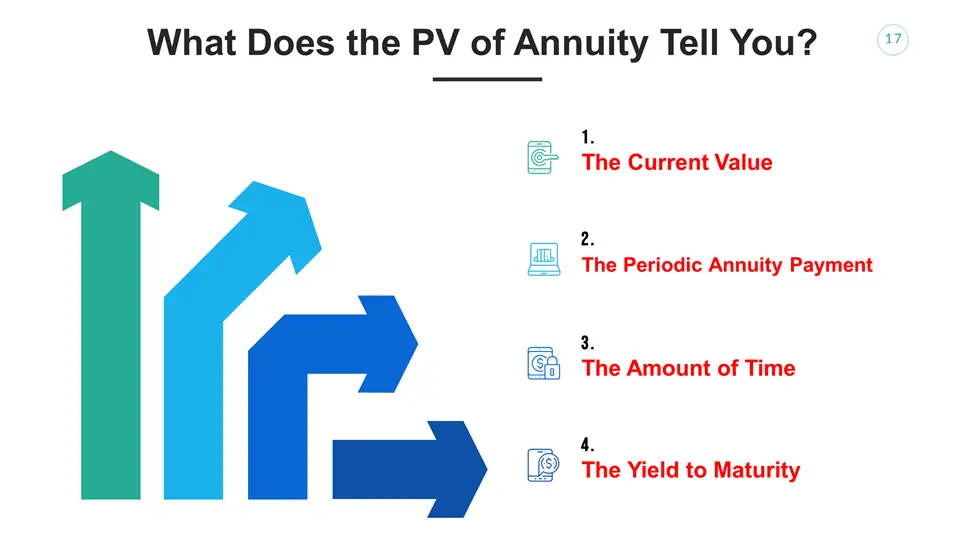

What Does the P.V. of Annuity Tell You?

The P.V. of annuity tells you the following:

- The Current Value

- The Periodic Annuity Payment

- The Amount of Time

- The Yield to Maturity

Frequently Asked Questions

How do determine an annuity’s present value?

By calculating its present value, you may determine the worth of all the income that an annuity is anticipated to provide in the future (P.V.).

The computation considers both your monthly payment and the rate of interest the annuity delivers. In addition to the number of periods, often months, that you anticipate paying into the annuity, this is also necessary. The P.V. calculation represents the time-value-of-money principle, which states that a dollar earned now is worth more than one earned tomorrow.

The P.V. calculation applies a discount to prepayments based on the number of payment periods. So, to get the present value of an annuity, use the following formula:

PV of annuity = P * [1 – ((1 + r) (-n))] / r.

- Periodic Payment = P

- Periodic interest rate = r

- n = the number of cycles

The payment and interest rate are presumptive constants throughout the life of the annuity installments in this equation.

How to calculate the present value of a pension?

The present value of a pension is calculated as PV = FV / (1 + i)^n.

The statement is true when the current value is equal to the future value multiplied by one plus the anticipated interest rate over the next “n” years.

How to calculate the present value of an ordinary annuity using a basic calculator?

With any calculator that contains an exponential function, even the most basic ones, you can calculate the P.V. of a standard annuity.

Calculators are useful because they have distinct keys for each variable in time-value-of-money calculations.

In all, you can calculate the present value of an ordinary annuity using the basic calculator below. We will use this example: If you need to find the present value of an ordinary annuity using a P.V. of 10,000 at 10% in 8 years. You can calculate this using a basic calculator through the following steps:

- Enter the value of the interest rate in decimal form. Using the example above, that will be 1.10.

- Press the division sign twice.

- Press the equal sign once

- Press the equal sign again, depending on the number of years in the problem. From the example, you will have to press it 8 times, since we have been working for 8 years.

- You will then get the present value. From the example above, this will be 0.466.

- Multiply this result by the P.V. value. From the example above, this will be 10,000.

- Press the equal sign to get the final Present value. From the example above, this will be 4665.073.

How much does a $50 0000 annuity pay per month?

If you buy a $50,000 annuity at age 60 and start receiving payments right away, you would get around $219 each month for the rest of your life.

How much does a $1000000 annuity pay per month?

You may anticipate receiving between $4,000 and $5,500 per month if you buy your $1,000,000 annuity between the ages of 60 and 70 and begin receiving payments immediately. This often lasts for the remainder of your life or the duration of your annuity payment.

Should a 70-year-old buy an annuity?

Yes. According to many financial consultants, starting an income annuity between the ages of 70 and 75 may optimize your payoff. Typically, deferred income annuities only take 5 to 10% of your money and start paying off later in life.

Can I live off the interest on a million dollars?

S&P annualized returns have historically averaged 9.2%. Therefore, if you invest $1,000,000 in stocks, you will get $96,352 in interest per year. Most people can survive on this amount.

Can you live off the interest of 2 million dollars?

Yes, it is the solution. If wise, you could live off the interest on $2 million.

What percentage of retirees has a million dollars?

According to a United Income survey, one in six retirees had $1 million in assets.

Expert Opinion

One use of the time worth of money is the annuity payout. The discrepancy among annuity payments based on regular and due annuity further supports this. Since the revenue is paid at the beginning of each month, an annuity has a reduced payment. It is anticipated that the money will be invested in the market, during which interest will be generated.

A present value annuity calculator is also useful for determining how much capital would be required today to finance a series of prospective annuity payments. An amount of money received now is worth more than a similar quantity later due to the cash’s time value. At this point, the present value of an annuity calculator will be your best ally.

References