Information presented on this web page is intended for informational and educational purposes only and is not meant to be taken as legal, financial, investment or tax advice. We do not accept any responsibility for any trading or investment related losses. Please review our disclaimer on before taking action based upon anything you read or see.

Debt may take many forms, including credit cards, mortgages, auto loans, school loans, etc. Additionally, it has a horrible habit of pleading for attention. However, paying off your debt doesn’t have to absorb you completely. The early debt payoff calculator is a fantastic tool for aiding with debt repayment. This will also enable you to enjoy the ease of a life without debt.

Additionally, the amount of personal debt in the US reached over $14 trillion as of the first part of 2022. Many Americans experience severe financial troubles due to their mountainous debt regardless of age, education, or income level. Debt may put you in considerable financial problems, whether you have credit card payments, school debts, or an expensive home.

You should make every effort to pay off your debts as fast as you can since being in debt may be a slippery slope. It won’t be simple, but most banks let you pay off a debt early. You often have to pay a minimum amount each month toward that debt, which won’t help you pay it off quicker.

Learn how to repay debt early and when you ought to consider doing so if you want to be financially secure. The Early debt payback calculator will be of great use to you now. An early debt payback calculator is what?

Some folks just like the sense of debt freedom. If the money used to pay off the low-interest debt is invested in securities or other alternative assets, such as real estate, with predicted returns greater than the loan’s interest rate, it will work harder. Here, the early debt payback calculator often provides sufficient assistance.

How to Early Debt Payoff Calculator

You can use your early debt payoff calculator through the following steps:

- Enter your Existing Payment.

- Enter your Rate of Interest

- Put your Monthly Debts

- Enter your Frequency of Payments

- At this point, the early debt payoff calculator will process and give you the debt payoff output.

Early Debt Payoff Calculator

Why use an Early Debt Payback Calculator?

Paying off debt is often a wise decision when you have cash available. In addition to the psychological advantages of being debt-free, you experience substantial cash rewards. Paying debts early isn’t always the optimum plan, but it’s seldom disastrous.

Use the early debt payback calculator to assess your situation and choose what is best for you. This will also enable you to weigh those advantages against the price of maintaining existing debt. Some more valid reasons for using an early debt payoff calculator include:

1. Save money

The quickest way to pay off debt, save money, and avoid paying interest is to utilize an early debt payback calculator. You can only purchase time with interest costs. Spreading out the payments over many years allows you to purchase a house or automobile without paying the whole cost.

When you make payments on a mortgage, your home doesn’t become any larger. And when you sell, you don’t receive your interest back. So, it is advisable not to pay for any more time above what you need.

Some loans take 30 years or more to pay off, and the interest charges mount over time. Other loans may have shorter durations but are more costly due to their high-interest rates.

It almost seems obvious to pay off high-cost debt as soon as possible, such as credit card debt: Paying the bare minimum is also a terrible idea. If you use the early debt payment calculator to pay off debts sooner, you’ll retain more of your income throughout your lifetime.

2. Increase Financial Stability

After using the early debt payback calculator to reduce your debt, you’re in a better financial situation. Your previously dedicated monthly payment money becomes accessible for other purposes.

For instance, when you pay off a vehicle loan, you may use the money you pay each month into savings or repay other obligations.

As a lender, you also gain in appeal. Lenders want to ensure you have the resources to repay loans and that your current debt isn’t taking too much of your monthly income. To achieve this, they determine a debt-to-income ratio, the proportion of income used to pay off debt.

Early loan repayment raises your ratio, which increases your chance of being authorized for a new loan with favourable conditions.

Your credit scores may also rise when you reduce your debt with the early debt payback calculator. Your current debt load affects a portion of your credit score.

This relates to the largest amount you could be able to borrow. Your credit ratings will be worse if you have reached your credit limit. However, paying off debt releases the ability to borrow—which you ideally won’t need to utilize.

3. Mental calm

Paying off debt may be satisfying and stress-reducing. Even if they know it doesn’t make the most financial sense, some individuals opt to pay off debts as quickly as possible. That’s OK as long as you know your actions and motivations.

The cost of happiness is priceless. Maybe you’re weary of making monthly payments, you want to pay off your debt before retirement, or you detest the thought of paying interest to creditors. The early debt payback calculator’s benefits are quite significant. Making a choice that you can live with will be made easier for you as a result.

How much will you contribute each month?

The 20/10 rule states that your yearly take-home salary should not be more than 20% of your total consumer debt payments. This is a maximum of 10% of your monthly take-home pay. This advice may assist you in reducing your debt load, which is crucial for your credit score and financial stability.

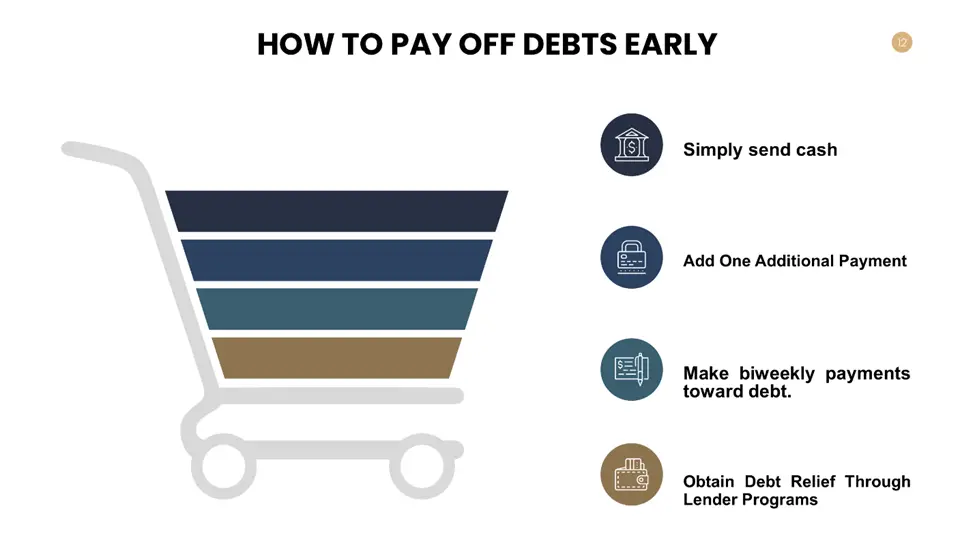

How to Pay Off Debts Early?

You may save a lot of money if you pay your bills as soon as possible. The motivation is there for a lot of folks. They also comprehend the significance of debt elimination. Most of the time, it’s merely a logistical issue.

You may pay off your debt in a few easy ways. Make sure you know how to pay off debt early with the specific lender you’re utilizing before you select one. For that lender to correctly credit goods, prepayment fees or other requirements can apply. However, you may Pay Off Debts Early by following this advice:

1. Simply send cash

Paying a little bit—or a lot—more each time you can is the easiest approach to getting out of debt sooner. Due to the need for discipline, it is also the most difficult to do. If you don’t believe you’ll adhere to the strategy, you may consider employing an automatic approach.

Just send additional payments if you want to wing it and are confident in your ability to pay off debts on your own. Include a memo section note with your check that reads, “Apply to the Principal.” Your creditor won’t be perplexed in this manner.

They’ll be aware that you’re making an additional payment, and they can get in touch with you if anything needs to be changed. After the first two or three repayments, follow up to confirm that your instructions were received and executed.

Payment systems generally feature space to put a remark about your intentions and follow the same principle.

2. Add One Additional Payment

A monthly pay increase can help you pay off your debt faster. If your monthly repayments are $1,200, make a one-time additional payment of $1,200. You may utilize money from a bonus or tax return.

It may be difficult to come up with the extra payment if you’re like most individuals. Spreading out the additional payment throughout the whole year is an option. Add the result to each monthly installment by dividing your payment by 12.

3. Make biweekly payments toward debt.

Alternatively, you may pay off your debt by making payments every two weeks instead of monthly. In the end, you’ll pay an additional amount every year. You should not notice a major shift in your monthly spending while paying off debt with biweekly payments. However, since you’ll be paying less interest as you repay the loan with time, you’ll experience significant savings.

4. Obtain Debt Relief through Lender Programs

To assist you in paying off debt more quickly, your borrower may offer you some choices. Be cautious since some programs could ask you to pay extra costs. Pay the fees if you think they are worthwhile. Find a method to pay more while eliminating the fees if you don’t like them.

You might configure automatic monthly payments in your bank’s online bill payment service. Don’t forget to include a letter stating, “Implement to the principal.”

Your lender isn’t the only business that will happily accept payment for a debt-reduction plan. They provide methods and software to manage everything for you. In general, unless they will assist in resolving a disciplinary issue, you don’t require these services.

Do whatever works, as long as you save so much money than you invest if there is no other way to get the job done.

Alternative Methods of Managing Mounting Debt

Managing increasing debt is a critical and significant part of operating your day-to-day company. Debt can have some positive aspects, but it also needs constant, frequent care. Controlling your debt is essential to your success as a company owner.

Your company will gain if everything is done well. If not, debt can become a problem. These Alternative Methods of Managing Mounting Debt have been gathered after an extensive study of different approaches and techniques. They consist of:

1. Be mindful of the conditions and interest rates in effect now and in the future.

Understanding precisely how it works and having the vision to anticipate how it will impact your organization in the future are the first steps you should take before taking on any debt. If you find yourself in debt with unfavourable terms, look for other options.

Compare prices! Look up and evaluate interest rates, then consider the ones most suited to your requirements. Understanding how interest rates may impact you is crucial.

For instance, if you take out a loan with a variable interest rate, the loan’s payment will fluctuate in line with market rates. You must determine if your investment will take on that amount of risk.

2. Enhance cash flow administration to prepare for payments

You should be able to set aside cash flow to pay off your debt after you’ve identified it and created a budget. Measuring and predicting cash flow, enhancing payables and receivables management, and being ready for gaps are necessary to boost cash flow.

These tactics don’t always represent answers, but they provide a chance to reduce some of the risks associated with debt for your company.

Cost-cutting measures are another method for enhancing cash flow. The more money that goes toward paying off your debt, the less money you spend overall.

It looks like a rather straightforward equation. Investors must be impartial when deciding which expenses to prioritize and where to make savings. Prioritizing your payments as your cash flow improves can help you first pay off your highest-risk debts, which also have the highest interest rates.

3. Think about debt relief

When used wisely, consolidating your debt may help you reduce your debt and improve your financial situation. Integrating your debt into a debt-consolidation loan offers a cheaper interest rate and quicker bill payment than paying off all of your debts individually.

If you’re thinking about consolidating your debt, it’s better to do it with the help of a financial counselor.

4. Assess your workspace; another cost-cutting approach is using extra space.

Look around your workspace and see if you can make any modifications. Is it operating as effectively as it could? If you have extra space, think about renting it out or selling it to generate more income so you can pay off your obligations and loans.

Conclusion

In conclusion, carrying debt is a big burden. The debt might make it difficult for you to accept fresh possibilities and make you feel pressured and unhappy. The Early debt payback calculator will be of great use to you now.

Expert Opinion

According to data, the typical American is in debt of $92,727. This covers outstanding mortgage, credit card, and student loan debt. It might seem challenging to manage your debt, regardless of whether it exceeds or falls below that sum.

Some solutions may assist you even if you’re having trouble paying off your debt and maintaining your financial stability. The exact tactics covered in this manual may be used. The early debt payoff calculator will help you make payments and free yourself from debt bonds.

References