Information presented on this web page is intended for informational and educational purposes only and is not meant to be taken as legal, financial, investment or tax advice. We do not accept any responsibility for any trading or investment related losses. Please review our disclaimer on before taking action based upon anything you read or see.

A credit card is a little plastic card issued by a bank, company, or other entity. This lets the bearer place orders or withdraw an interest-free loan on credit from the provider. A credit card’s credit limit, or the highest amount of credit it may issue, should not be exceeded. Here is the credit card payment calculator with interest.

A credit line fee may get charged if the credit card user exceeds the limit. The credit card user can repay the whole sum at the end of the month or leave an account debt that will accrue interest until it gets cleared off. Credit card interest rates are often higher than other loans, such as foreclosures, auto loans, and student loans.

As a result, the total should preferably get paid off regularly to prevent excessive interest rates. As a result, we’ve prepared this page on credit payment amounts to help you.

Furthermore, knowing how your credit payments are computed and allocated to your current obligations is crucial. This will assist you in keeping your total credit card debt under control.

By calculating the regular daily rate on your credit cards, you may better understand how compound interest affects how much you recoup in interest.

Your credit payments may get broken down into annual or monthly amounts on your monthly report, and you may break it down into a monthly APR. This data might assist you in determining which credit cards you should concentrate on paying off rapidly. This is in addition to how much it costs to borrow money from your card issuer daily.

How to Use this Credit Card Payment Calculator with Interest

You can use this credit card payment calculator with interest through the following steps:

Step 1: Enter the credit amount

Step 2: Enter the interest rate (in %)

No Step 3: Enter the credit term (in months)

Step 4: Click on “calculate”, and your monthly payments and total payments will be displayed upon calculation.

If you desire to re-calculate, click “reset”, and all your earlier inputs will get cleared.

Credit Card Payment Calculator with Interest

What is the Formula for a Monthly Credit Card Payment with Interest?

To calculate a monthly credit card payment with interest, divide the yearly rate by 12 to get a monthly rate. As there are 12 months per year, this is true. Multiply your amount owed by the monthly rate.

How to Calculate Interest Charges on Credit Cards

It would help if you first determine your APR to compute your credit card interest charges. This is in addition to your average daily balance and the number of days left in your pay period. Most of this data should be accessible by simply signing into your account.

- To calculate your regular daily rate, divide your annual percentage rate by 365 (the number of days in a year).

- Multiply it by your current mean balance. Your total amount divided by the number of days in your pay period is your total daily amount.

- To calculate your total interest costs for the pay period, multiply your regular daily rate by the number of days in the billing cycle.

- You will almost certainly get charged interest if you have a credit card bill. Credit card providers may allow you different amounts of time to pay for new transactions before charging interest. On the other side, they usually allow you a month to do the task.

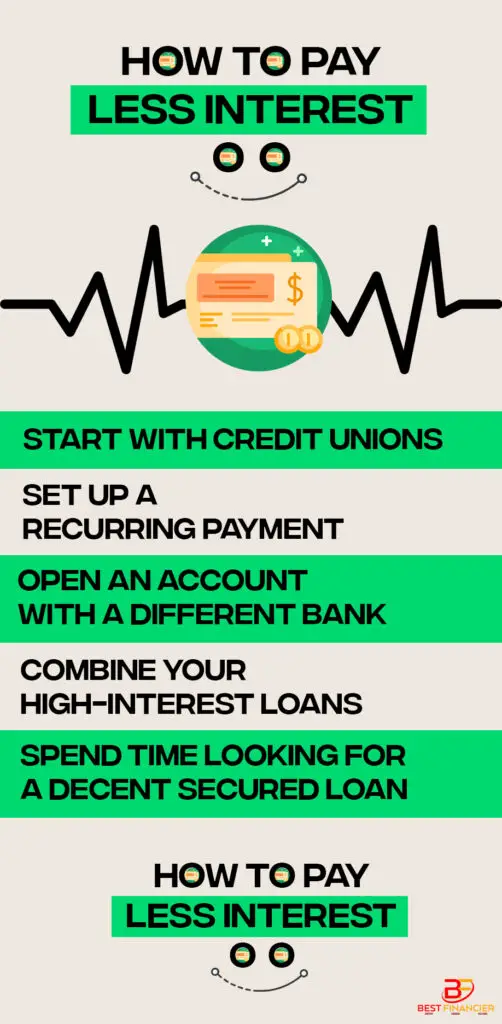

How to Pay Less Interest

These tactics will lead to significant savings on your loans, whether you are looking for a loan or want to locate better interest rates on your existing loans. The lower your interest rate, the less extra you will pay. However, it might impact the overall payment amount and the time it takes to pay off the loan. These loan solutions will work for the majority of your loans:

Start with credit unions.

Credit unions and local banks may provide cheaper interest rates on loans than bigger banks. It may require some digging, but if you can qualify for assistance via your local credit union, you could be able to cut your interest rate.

To obtain a loan from a credit union, you must be a member of the organization. This implies you must fulfill specific requirements, such as residing in a given place or working for a specified company.

Comparing the rates given by several local banks may save you much money in the long run, particularly on bigger loans like a mortgage. The bank’s current borrowing costs may be seen on the company’s website.

Set up a recurring payment

You could be able to decrease your interest rate if you set up direct debits. This method applies to personal loans, vehicle loans, and mortgages—banks like this since they are more certain to get paid on time when using this method.

You also do not have to be concerned about paying your monthly payment. Check your existing loans to determine whether you match this alternative.

A simple inquiry and follow-up to ensure the reduced interest rate will help you save money on your loan interest. It usually does not apply to credit cards, although periodic loans may be a possibility with your student debts.

Open an account with a different bank.

If you have a current account with a bank, you may be eligible for cheaper mortgage or vehicle loan rates. Switching banks may save you money, particularly if you have an enormous debt such as a mortgage. Regarding your mortgage, using a refinance that can assist you in obtaining the best conditions for your loan may be helpful.

A lender may be able to assist you in locating a credit that has this feature. Although switching accounts may seem inconvenient, having all your assets at one bank might make things easier.

Another alternative is to keep a profile up and make monthly loan payments to it. Ensure the checking account has no mandatory activity or balance limitations to prevent extra fees.

Combine your high-interest loans

Combine your higher-interest debts if at all feasible. Credit cards and low-interest personal loans fall under this category. Because you are not incurring as much monthly interest with these loans, you will be able to pay off your debt quicker. It might be an excellent alternative if you follow two simple rules.

To begin, you must entirely cease using your credit cards. Taking loans is pointless if you’re going to be in debt every month. Second, you should avoid using a mortgage debt line or a home loan to get a refinance loan. It jeopardizes your house if you cannot pay your bills in the future.

Spend time looking for a decent secured loan.

You may save a lot of money with an intelligent consolidation loan. Also, double-check that you will not be utilizing your credit cards before you do anything. Before you pick out the secured loan, you may want to make a target of never using them for two months to break the habit.

How to Calculate your Monthly APR

In three simple steps, you may calculate your monthly APR rate:

- Step 1: Check your credit card bill for your present APR and amount.

- Step 2: To calculate your monthly recurring rate, split your present APR by 12 (for the 12 months of the year).

- Step 3: Multiply that quantity by the existing balance amount.

How to Calculate Your Daily APR on a Credit Card

Your credit card firm may use a daily periodic rate to compute your interest.

In three simple steps, you may determine your daily APR:

- Step 1: Check your credit card bill for your present APR and amount.

- Step 2: To calculate your regular daily rate, divide your annual percentage rate by 365 (the number of days in a year).

- Step 3: Take your current balance and double it by the regular daily rate.

Frequently Asked Questions

Will I have to pay Annual Percentage Rate charges?

There’s no need to worry about your APR if you repay on time and in full. On the other hand, your APR is essential if you don’t pay your debt in full. Most credit cards have APRs of 20% to 30%, implying you might wind yourself paying significantly more in the long run.

Why should I know my daily and monthly APR?

By computing your daily and monthly APR, you may start understanding how much of your cash goes to interest. Knowing how much of your funding goes to interest instead of your principal might help you pay off your debt faster. This will also assist you in determining whether goods are worthwhile to charge to your credit card.

How much interest will I pay on my credit card balance?

Divide the card’s APR by 365 to determine how much interest you’ll pay on your credit card. Then divide the value by your current average balance and the duration of the billing cycle. Your monthly credit card bill will also include the interest rates you owe.

What is 24% APR on a credit card?

A credit card with a 24 percent APR means that the rate you pay over a year is approximately 24 percent of your balance. If your APR is 24% and you have a $1,000 amount, you will owe $236.71 in the rate at the end of the year.

How is using a credit card similar to taking out an interest-free loan?

Credit cards may easily get used as a brief loan, but those that give 0% APR for a specific timeframe might be considered “free.” The secret to utilizing a credit card as an equity loan is to make sure you can clear off your whole debt before the promotional offer on your card expires.

How can I avoid paying interest on my credit card?

The following methods may help you avoid paying interest on your credit card:

- Always pay off your credit card balance in full each month.

- Use a stored value card to consolidate debt.

- Make significant purchases with caution.

- Make use of a debt payback strategy.

- Use your money to pay off your debt.

- Make numerous monthly credit card payments.

- Take out a personal loan.

How much is the total interest paid?

The total interest paid during the life of a credit or equity account is the aggregate of all interest paid. Cumulative amounts on unpaid cumulative interest get included. The expression [Total Liabilities Amount] = [Principle] + + [Interest on Late fee] may be used to calculate it.

How long would it take to pay off a credit card balance of $15 000, paying just minimum payments?

On a $15,000 debt, a minimum monthly payment of 3% per month is 227 months (approximately 19 years) of repayments, beginning at $450 monthly. You’ll have paid approximately more in interest ($12,978 if you’re taking the annualized return of 14.96 percent) than you did in principle when you’ve completed the $15,000.

Is 24.99 APR good?

However, a 24.99 percent APR is appropriate for private loans and credit cards, especially for persons with poor credit. If at all possible, you should avoid accepting a rate this high. A credit card with a 24.99 percent APR is respectable but not optimal. A credit card’s median annual percentage rate (APR) is 18.32 percent.

Is a 9.99 APR good?

Any credit card interest rate under 14 percent is considered favorable. For persons with great credit, this is around the average regular interest rate on credit cards. Furthermore, even a respectable credit card interest rate for folks with poor credit scores isn’t that terrible.

What is an excellent credit score?

Credit scores of 800 and higher typically get regarded as outstanding. However, boundaries vary based on the credit scoring algorithm.

How is interest calculated in interest?

You can do it by multiplying the lending rate in decimal notation to compute interest charges by one. Next, multiply this answer by the primary amount to get the total number of composite periods. The initial principal amount gets deducted from the outcome.

How is interest charged on a credit card?

Interest on a credit card gets calculated according to the conditions of your cardholder contract. It gets determined as a daily rate by splitting your yearly marginal rate by 365 and multiplying your actual amount by the standard rate, and that proportion then increases your bill.